As many countries across the globe shift from public-led stimulus to private-led debt to reduce the impact of COVID-19 on the financial system, the burden to keep the economy running will largely fall to private lenders. U.S. banks will set aside up to $320 billion to cover potential credit losses in 2020 due to the financial strain of the pandemic, according to a new report from Accenture (NYSE: ACN).

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20200728005228/en/

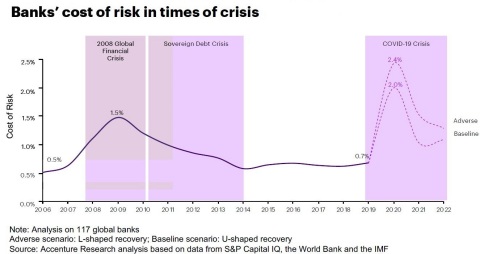

Banks’ cost of risk in times of crisis

Titled “How Banks Can Prepare for the Looming Credit Crisis,” the report projects that banks globally will set aside up to 2.4% of their existing credit books to cover expected losses in unpaid loans ―nearly double what banks wrote off during the 2008 global financial crisis. The impact will vary across the globe depending upon the level of government-funded stimulus programs and the severity of the public health aspect of COVID-19. In the U.S., around 9% of home loans were in forbearance as of June, up 6 percentage points since March. In the U.K., payment holidays were issued on one in six mortgages and 1.5 million credit cards and personal loans.

“Banks will play a critical role in helping absorb the economic impact of the global pandemic and stimulating a rapid recovery for consumers and small businesses,” said Alan McIntyre, a senior managing director at Accenture who leads its Banking practice globally. “As public programs wind down, the burden of holding extra capital to protect against credit defaults will fall on banks’ balance sheets. To inform their credit management strategies, banks will need a clear-sighted and data-driven view of the current level of credit risk while keeping a long-term view of the customer at the forefront.”

In 2019, U.S. banks set aside US$55 billion to cover potential loan losses; Accenture estimates that banks will need to hold an additional US$210 billion to US$265 billion to cover potential write-offs for bad loans in 2020 depending on the severity of the public health aspect of COVID-19. In Europe, banks might write off up to US$460 billion in 2020, an increase of US$370 billion from 2019; and in China, banks might write off up to US$360 billion in 2020, a US$190 billion increase from 2019.

In the increasingly debt-driven economy, banks are faced with managing their existing loan books while also making decisions around extending new credit. The report notes that doing so could lead to record levels of public and private debt worldwide, which some analysts predict could reach as high as $200 trillion by the end of 2020. This might ultimately threaten the ability of businesses and consumers to repay their debts.

Large banks in a position of strength when the pandemic hit

Many banks entered the pandemic with the financial resilience to absorb considerable credit losses, with the world’s largest banks holding capital reserves well above what regulators require, according to Accenture analysis. The report notes that the top five U.S. banks set aside US$60 billion in reserves during the first half of the year and that European banks set aside almost US$18 billion in the first quarter of 2020. These reserves will start to be drawn down as stimulus funding dries up, causing accounts to go delinquent.

“Banks will have to maneuver carefully to strike the right balance between rescuing individual and small business customers and protecting their own profitability and solvency,” McIntyre said. “This will require difficult decisions around which credit extensions will help an ultimately financially viable customer versus delaying the inevitable delinquency. To make these decisions, banks can apply the firepower of data and analytics capabilities that they’ve built over the past decade to help inform surgical credit management strategies tailored for specific industries and geographies ―ultimately providing the type of high-end treatment typically reserved for high-net-worth and corporate customers.”

Banks’ temporary blind-spot in credit management

The report notes that in an environment where payment holidays aren’t being reflected in consumers’ credit scores and the underlying health of a business is masked by furlough and payroll protection schemes, banks can take a data-driven approach to manage their credit portfolio. This approach can provide a broader context of the current environment and how business and consumer behaviors have changed as a result of COVID-19.

Over the past decade, banks’ credit management units have shrunk back to bare bones. Many banks will need to quickly scale up resources and collections capabilities to a magnitude beyond what they can traditionally handle to meet the expected rising levels of default. By combining the digital technologies they’ve built over the past decade with their people on the front lines, banks can provide personalized advice and empathetic guidance to offer creative solutions to help customers bridge the widening financial gap.

The report provides recommendations for how banks can strengthen their credit management capabilities and prepare their business and operations for the challenges to come, while managing potentially conflicting priorities. These include:

- engaging with regulators to avoid/minimize unintended consequences such as new credit drying up;

- operating with clear guidance and transparency on collections and recovery;

- ensuring fair treatment for borrowers while also having a clear view of customers’ creditworthiness; and

- managing balance sheet risk while providing advice that helps businesses and consumers navigate through the financial crisis.

“While it might be tempting for banks to pull back on extending new credit in the current environment, the demand for credit will rise and be met ― if not by banks then by non-traditional lenders,” McIntyre said. “Competition isn’t coming just from fintechs and big tech, but increasingly from large, well-capitalized companies offering finance options for their products and services. If banks attempt to aggressively reduce offers of credit, what might start as a slow trickle of customers turning to alternate lenders could quickly become roaring rapids that can drastically change the tide of lending.”

The full report can be accessed here: https://www.accenture.com/us-en/insights/banking/coronavirus-credit-crisis.

About Accenture

Accenture is a leading global professional services company, providing a broad range of services in strategy and consulting, interactive, technology and operations, with digital capabilities across all of these services. We combine unmatched experience and specialized capabilities across more than 40 industries – powered by the world’s largest network of Advanced Technology and Intelligent Operations centers. With 513,000 people serving clients in more than 120 countries, Accenture brings continuous innovation to help clients improve their performance and create lasting value across their enterprises. Visit us at www.accenture.com.

View source version on businesswire.com: https://www.businesswire.com/news/home/20200728005228/en/