The “global finished vehicle logistics market 2019-2023” report has been added to Technavio’s catalog.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20190917005724/en/

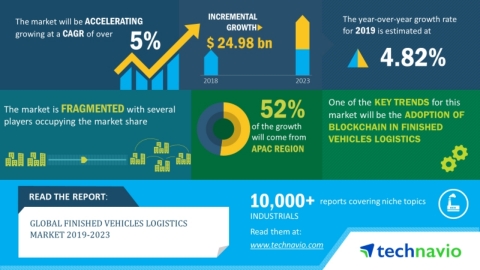

Technavio has announced its latest market research report titled global finished vehicles logistics market 2019-2023. (Graphic: Business Wire)

The global finished vehicle logistics market is expected to increase at a CAGR of over 5% during 2019-2023.

The finished vehicle logistics market deals with several activities including port processing, yard management, claims management, and inspections. All these activities occur during the time the vehicle leaves the factory to reach the dealer. Several factors including the rapid digital transformation in finished vehicle logistics and the emergence of electric vehicles are aiding the finished vehicle logistics market. Finished vehicle logistics market is segmented into road, rail, sea, and air depending on the mode of transportation mode employed.

For more Information get Free Sample Report

The rising popularity of multimodal transport of vehicles is one of the critical factors contributing to the overall expansion of the finished vehicle logistics market during the next few years. High demand from the automotive sector has boosted the use of multimodal transport for finished vehicles logistics as it helps to reduce transportation costs and drives efficiency. Many companies have also started using customized solutions for transporting vehicles. This has further led to the launch of various government initiatives and tax reforms, facilitating the growth of the multimodal transport of finished vehicles. Such initiatives are expected to fuel the growth of finished vehicles logistics market during the next few years.

The use of blockchain technology in the finished vehicle logistics systems is one of the key trends that will trigger market growth in the upcoming years. Companies are using this technology to execute efficient and cost-saving business operations for finished vehicles logistics. Blockchain technology also helps in streamlining freight transactions while improving the visibility, security, and accuracy of data. Several market players are deploying this technology to track each vehicle unit in real-time and automate administrative transactions.

Regional Outlook

The global finished vehicles logistics market spans across five major regions of the globe: APAC, North America, Europe, MEA, and South America. The finished vehicle logistics market in APAC is the fastest-growing market globally, with an incremental growth of USD 12.98 billion during 2019-2023.

China is expected to account for the highest finished vehicles logistics market share due to the flourishing automotive market in the country. Furthermore, various automobile manufacturers are establishing new production plants in India and China. With the rise in automotive production and sales, there will be a proportional rise in the demand for finished vehicle logistics across these emerging economies.

Competitive Outlook

Ceva Logistics AG is a Switzerland-based company operating in key business segments including freight management and contract logistics. The company holds a significant presence in EMEA, Americas, and APAC. With an employee strength of 58,000 and overall revenue of close to USD 7.35 billion, the company has been offering finished vehicle logistics services including customs brokerage and compliance, pre-dispatch inspection, export compliance and management, storage center operations, and support diagnostics.

Get Full Report: https://www.technavio.com/report/finished-vehicles-logistics-market-industry-analysis

Key Topics Covered:

1. Executive summary

1.1. Contribution of market under focus to the parent market

1.1.1. Parent market

1.1.2. Market in focus

1.2. Growth momentum

1.2.1. Year over year growth

1.3. Market share by region

1.4. Incremental growth

1.4.1. Global market growth

1.4.2. Contribution to the global market growth by region

1.5. Market share by transportation mode

1.6. Market share of key countries in 2018

1.7. Structure of the market in focus

1.7.1. Market concentration

1.7.2. Market maturity

1.7.3. Market participants

1.8. Factors that are driving demand

1.9. Challenges that affect the market dynamics

1.10. Key trends that are impacting the market

2. Scope of the report

2.1. Preface

2.1.1. Market definition

2.1.2. Objectives

2.1.3. Notes and caveats

2.2. Currency conversion rates for US

3. Market landscape

3.1. Market ecosystem

3.1.1. Global logistics market

3.1.2. Segments of global logistics market

3.2. Market characteristics

3.2.1. Market characteristics analysis

3.3. Market segmentation analysis

4. Market sizing

4.1. Market definition

4.1.1. Parent market

4.1.2. Market in focus

4.1.3. Segmentation

4.1.4. Methodology for market sizing and vendor selection

4.1.5. Market definition – Inclusions and exclusions checklist

4.2. Market sizing 2018

4.3. Market size and forecast 2019-2023

4.3.1. Global market: Size and forecast 2018-2023 ($ millions)

4.3.2. Global market: Year-over-year growth 2019-2023 (%)

5. Five forces analysis

5.1. Five forces analysis 2018

5.2. Five forces analysis 2023

5.3. Bargaining power of buyers

5.4. Bargaining power of suppliers

5.5. Threat of new entrants

5.6. Threat of substitutes

5.7. Threats of rivalry

5.8. Market condition

6. Customer landscape

6.1. Customer landscape analysis

7. Market segmentation by Geography

7.1. Market share by geography

7.2. Geographic comparison

7.3. APAC

7.3.1. APAC – Market size and forecast 2018-2023 ($ millions)

7.3.2. APAC – Year-over-year growth 2019-2023 (%)

7.4. North America

7.4.1. North America – Market size and forecast 2018-2023 ($ millions)

7.4.2. North America – Year-over-year growth 2019-2023 (%)

7.5. Europe

7.5.1. Europe – Market size and forecast 2018-2023 ($ millions)

7.5.2. Europe – Year-over-year growth 2019-2023 (%)

7.6. MEA

7.6.1. MEA – Market size and forecast 2018-2023 ($ millions)

7.6.2. MEA – Year-over-year growth 2019-2023 (%)

7.7. South America

7.7.1. South America – Market size and forecast 2018-2023 ($ millions)

7.7.2. South America – Year-over-year growth 2019-2023 (%)

7.8. Key leading countries

7.9. Market opportunity

8. Market segmentation by transportation mode

8.1. Market share by transportation mode

8.2. Comparison by transportation mode

8.3. Road

8.3.1. Road – Market size and forecast 2018-2023 ($ millions)

8.3.2. Road – Year-over-year growth 2019-2023 (%)

8.4. Rail

8.4.1. Rail – Market size and forecast 2018-2023 ($ millions)

8.4.2. Rail – Year-over-year growth 2019-2023 (%)

8.5. Sea

8.5.1. Sea – Market size and forecast 2018-2023 ($ millions)

8.5.2. Sea – Year-over-year growth 2019-2023 (%)

8.6. Air

8.6.1. Air – Market size and forecast 2018-2023 ($ millions)

8.6.2. Air – Year-over-year growth 2019-2023 (%)

8.7. Market opportunity by transportation mode

9. Decision framework

10. Drivers and challenges

10.1. Market drivers

10.1.1. Growing automotive industry

10.1.2. Global expansion of automobile manufacturing plants

10.1.3. Rise in popularity for multimodal transport of vehicles

10.2. Market challenges

10.2.1. Shortage of truck drivers

10.2.2. Inadequate logistics infrastructure

10.2.3. High operational costs

10.3. Impact of drivers and challenges

11. Market trends

11.1. Emergence of electric vehicles

11.2. Adoption of blockchain in finished vehicles logistics

11.3. Digital transformation in finished vehicles logistics

12. Vendor landscape

12.1. Overview

12.2. Landscape disruption

12.3. Competitive Scenario

13. Vendor Analysis

13.1. Vendors covered

13.2. Vendor classification

13.3. Market positioning of vendors

13.4. APL Logistics Ltd.

13.4.1. Vendor overview

13.4.2. Service segments

13.4.3. Organizational developments

13.4.4. Key offerings

13.5. ARS Altmann AG

13.5.1. Vendor overview

13.5.2. Business segments

13.5.3. Organizational developments

13.5.4. Key offerings

13.6. CEVA Logistics AG

13.6.1. Vendor overview

13.6.2. Business segments

13.6.3. Organizational developments

13.6.4. Geographic focus

13.6.5. Segment focus

13.6.6. Key offerings

13.7. Ekol Lojistik AS

13.7.1. Vendor overview

13.7.2. Business segments

13.7.3. Organizational developments

13.7.4. Segment focus

13.7.5. Key offerings

13.8. GEFCO Group

13.8.1. Vendor overview

13.8.2. Business segments

13.8.3. Organizational developments

13.8.4. Geographic focus

13.8.5. Segment focus

13.8.6. Key offerings

13.9. Koopman Logistics Group BV

13.9.1. Vendor overview

13.9.2. Business segments

13.9.3. Organizational developments

13.9.4. Key offerings

13.10. Kuehne + Nagel International AG

13.10.1. Vendor overview

13.10.2. Business segments

13.10.3. Organizational developments

13.10.4. Key offerings

13.11. OMSAN Logistics

13.11.1. Vendor overview

13.11.2. Service segments

13.11.3. Organizational developments

13.11.4. Geographic focus

13.11.5. Segment focus

13.11.6. Key offerings

13.12. Sevatas

13.12.1. Vendor overview

13.12.2. Service segments

13.12.3. Organizational developments

13.12.4. Geographic focus

13.12.5. Segment focus

13.12.6. Key offerings

13.13. Yusen Logistics Co. Ltd.

13.13.1. Vendor overview

13.13.2. Business segments

13.13.3. Organizational developments

13.13.4. Geographic focus

13.13.5. Segment focus

13.13.6. Key offerings

14. Appendix

14.1. Research Methodology

14.1.1. Research framework

14.1.2. Validation techniques employed for market sizing

14.1.3. Information sources

14.2. List of abbreviations

For more information about this report visit https://www.technavio.com/

View source version on businesswire.com: https://www.businesswire.com/news/home/20190917005724/en/